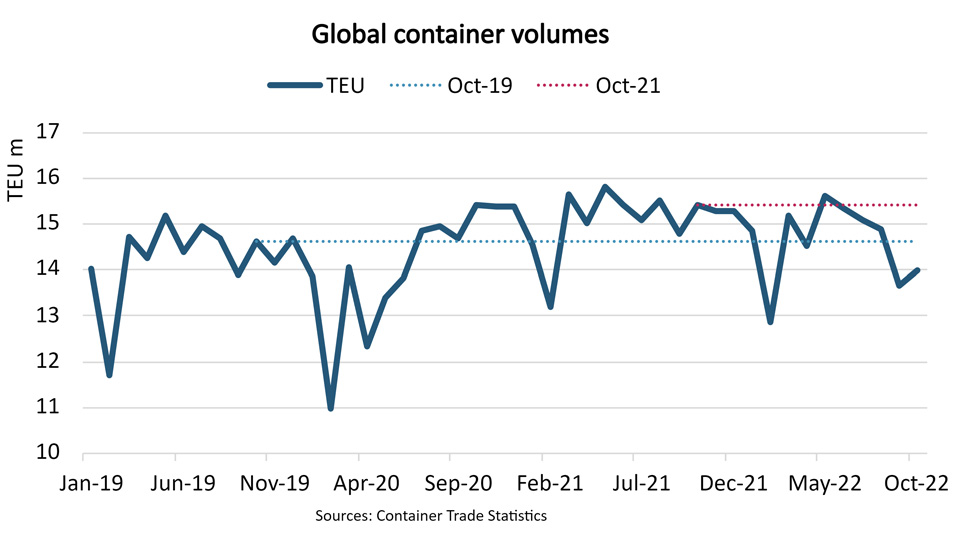

Global container volumes fall 9.3% y/y as historic growth cycle ends

From mid-2020, global container export volumes saw strong growth, and combined with increasing port congestion it caused supply chain challenges and historically high liner operator financial results which have been the norm since. In September 2022, however, container volumes dropped below volumes recorded in the same month in 2019 for the first time since mid-2020 and statistics just released by Container Trade Statistics have confirmed the trend.

In October 2022, global container export volumes fell 9.3% y/y and ended 4.3% lower than in October 2019.

Twenty out of twenty-eight region to region trade lanes ended with lower volumes than in October 2021 while eighteen trade lanes saw volumes lower than in October 2019.

Out of seven regions, five ended with lower import volumes in October 2022 than in October 2019. The Far East, Europe/Mediterranean, and North America regions combined import 75% of global container volumes and saw volume reductions of respectively 5.0%, 11.0%, and 0.4% versus October 2019.

The container fleet has grown 11.3% since October 2019, which helps explain why container freight and time charter rates have fallen so quickly during 2022, and particularly in recent months. The lower container volumes have also led to several service closures and an increase in blanked sailings. As a result, port congestion is improving quickly and no longer restrains supply to the extent seen during the past eighteen months.

The global economy is expected to end 6.2% higher in 2022 than in 2019 while global container volumes appear likely to end only between 1.0% and 1.5% higher than in 2019. This underlines the effects of the cost-of-living crisis across the world but volumes in recent months also indicate that inventory adjustments are driving volumes lower.

It now appears likely that global container volumes in 2022 will end approximately 4% lower than in 2021. Growth prospects for 2023 also appear weak due to weak prospects for global economic growth. At the same time, high contracting of new ships by liner operators during 2021 and 2022 indicates fleet growth of nearly 8% in 2023. All in all, 2023 is much more likely to see the beginning of a new normal rather than a reverse of the recent weakening of the supply/demand balance.

Feedback or a question about this information?

Posted:

07 December 2022

BIMCO's Shipping number of the week

- Container ship fleet expands by 11%, fastest growth in 15 years

- Dry bulk newbuild contracting fell 34.2%, despite a strong market

- Newbuilding prices climb 3% to highest level in 16 years

- Charter owners’ share of fleet has fallen to 40%, lowest since 2002

- Dry bulk sailing distances jump 31% for routes using the Panama Canal

ELSEWHERE ON BIMCO

Contracts & Clauses

All of BIMCO's most widely used contracts and clauses as well as advice on managing charters and business partners.

Learn about your cargo

For general guidance and information on cargo-related queries.

BIMCO Publications

Want to buy or download a BIMCO publication? Use the link to get access to the ballast water management guide, the ship master’s security manual and many other publications.