China’s July crude oil imports hit 4-year low and drops 9.2% y/y

China is the world’s largest importer of crude oil, accounting for approximately 25% of global crude import volumes. The country’s crude imports are also equal to about 25% of global seaborne crude oil volumes which contributed to about 30% of dirty tanker trade tonne miles in 2021 according to Signal Ocean statistics. From 2010 to 2020, China’s crude imports grew at an average annual rate of 8.5% and have been the key demand driver for both crude oil and crude tanker demand.

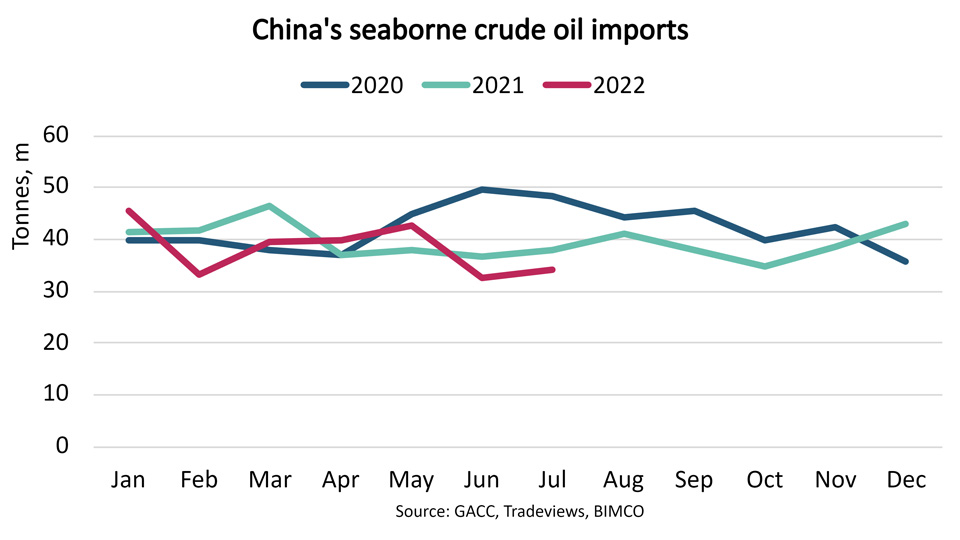

According to the General Administration of Customs China (GACC), crude oil volumes in July amounted to 34.1 million tonnes. Volumes are thereby down 9.2% on 2021 and 27.2% lower than July 2020. January through July 2022 volumes have fallen 3.9% compared to the same period in 2021 which was already down 5.7% against 2020.

Seaborne volumes have fallen similarly, however, dirty tanker trade deadweight tonne miles have dropped 9.6% in the first seven months of 2022 compared to last year according to Signal Ocean statistics. Compared to 2021, China has this year favoured imports from the Persian Gulf, Southeast Asia, and Russia over crude from Brazil, USA, and West Africa. On average, longer trades have been replaced by shorter ones.

VLCCs and Suezmaxes have both seen a reduction in deadweight tonne miles of about 10% January through July, whereas Aframaxes have benefitted from the increased trade with Russia and deadweight tonne miles have increased 1.5% year-to-date.

Crude oil demand in China has suffered from low local demand due to COVID-19 lockdowns. A combination of high product inventories, a cap on retail gasoline and diesel prices once crude hits USD 80/barrel, and lower export quotas (so far 39% lower than in 2021) that discourage refineries from ramping up production has also hurt demand for crude oil.

Deadweight tonne miles indicate it is unlikely that August’s import numbers will improve significantly whereas a rebound may be seen in September, although not to the highs of 2020. That would likely require both a solid increase in local product demand and changes in the policies that currently discourage refineries from increasing production.

Feedback or a question about this information?

Posted:

25 August 2022

BIMCO's Shipping number of the week

- Dry bulk newbuild contracting fell 34.2%, despite a strong market

- Newbuilding prices climb 3% to highest level in 16 years

- Charter owners’ share of fleet has fallen to 40%, lowest since 2002

- Dry bulk sailing distances jump 31% for routes using the Panama Canal

- Peak in China’s coal demand in sight as renewables jump 12%

ELSEWHERE ON BIMCO

Contracts & Clauses

All of BIMCO's most widely used contracts and clauses as well as advice on managing charters and business partners.

Learn about your cargo

For general guidance and information on cargo-related queries.

BIMCO Publications

Want to buy or download a BIMCO publication? Use the link to get access to the ballast water management guide, the ship master’s security manual and many other publications.