- Dry bulk newbuild contracting fell 34.2%, despite a strong market

- Newbuilding prices climb 3% to highest level in 16 years

- Charter owners’ share of fleet has fallen to 40%, lowest since 2002

- Dry bulk sailing distances jump 31% for routes using the Panama Canal

- Peak in China’s coal demand in sight as renewables jump 12%

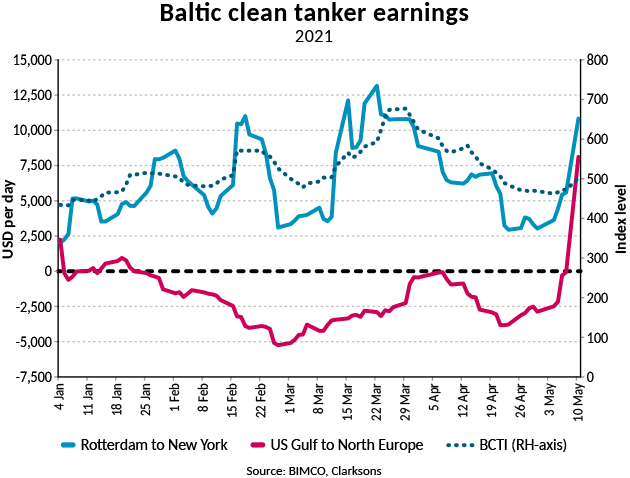

Clean product tanker rates on US bound trade almost doubles after pipeline attack

The closure of the Colonial pipeline which runs from the US Gulf to the US East Coast, has caused a spike in oil product tanker rates on trades to and from the region.

Earnings on the Rotterdam to New York trade for a Handysize tanker capable of carrying about 280,000 barrels of oil, jumped from USD 5,591 per day on 7 May to USD 10,833 on 10 May. This is because gasoline is in high demand and gas stations are being emptied by consumers worried about supply.

An even more impressive increase came on the US Gulf to North Europe trade where rates rose from negative USD 65 per day on 7 May to USD 8,118 per day on 10 May.

Though the higher rates on these two routes have pulled the basket BCTI index up, earnings on other benchmark trades outside of this region have not yet been affected, with the Baltic Clean Tanker Index (BCTI) posting a much more modest increase over the weekend of 6.4%.

Tanker shipping ready to step in to avoid shortages

The pipeline plays a major role in the US East Coast’s oil infrastructure, connecting the large refinery capacity in the Gulf Coast with the demand hubs along the East Coast with its 2.5m bpd capacity. Small parts of the pipeline are now said to be running again, but the main pipeline remains shut down as of early afternoon CET on 12 May.

Tanker shipping presents an obvious alternative to the pipeline; the longer the disruption, the better for the tanker shipping market, which its current state needs all the help it can get. This would either be by transporting the oil products from the refineries in the US Gulf to the consumers along the East Coast, especially if the Jones Act be waived, as this would allow foreign ships to complete the domestic voyage. Or by transporting more volumes across the Atlantic, should demand for on this trade pick up as a result of the pipeline closure. The latter would be preferable for the global tanker shipping industry.

Based on Signal Group data there are currently 38 ships available for the North Europe to US Atlantic trade and 56 on the US Gulf to North Europe route.

“Though on a different scale, the sudden jump in freight rates on these two routes mirrors developments after the US sanctions imposed in October 2019, as well as the breakout of the oil price war in March 2020. It reinforces the importance of geopolitics and shocks to the tanker market and their potential to bring earnings out of a slump, even if only temporarily, as is likely to be the case this time,” says Peter Sand, BIMCO’s Chief Shipping Analyst.

Posted:

12 May 2021

BIMCO's Shipping number of the week

ELSEWHERE ON BIMCO

Contracts & Clauses

All of BIMCO's most widely used contracts and clauses as well as advice on managing charters and business partners.

Learn about your cargo

For general guidance and information on cargo-related queries.

BIMCO Publications

Want to buy or download a BIMCO publication? Use the link to get access to the ballast water management guide, the ship master’s security manual and many other publications.