September head-haul volumes fall 15.5% y/y as liner landscape faces change

In September 2022, head-haul and regional export volumes were down 9.3% y/y according to Container Trade Statistics. Head-haul trades fell 15.5% whereas regional trades were down 0.7%. At the same time, volumes were 0.2% lower than in September 2019. The volume decline represented the first month since June 2020 to see lower volumes compared with the same month in 2019 and could be a warning that laid up ships and further freight rate reductions are on the horizon.

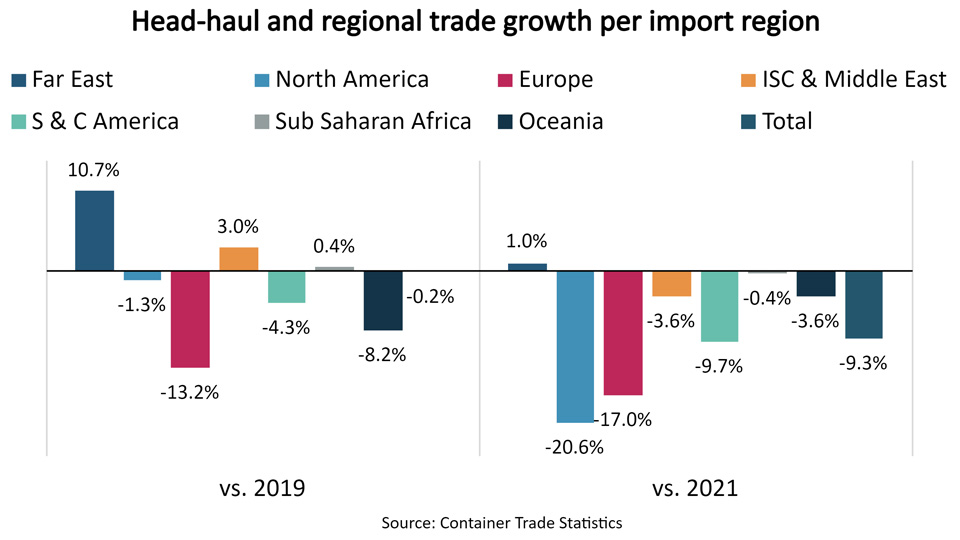

In September 2022, head-haul and regional trade volumes were lower than in 2021 into all import regions except the Far East. Remarkably, volumes into North America, which led the surge in volumes during COVID, saw the greatest loss at -20.6% y/y.

For container shipping the head-haul and regional trade volumes are the key drivers of ship demand and profitability. A head-haul trade is the direction of an interregional trade with the highest volume, such as Far East to North America. A regional trade is an intraregional trade such as within Asia. During 2021 and 2022 the head-haul and regional trades have also been the drivers of port congestion, which further increased ship demand and tightened the supply/demand balance in favour of the liner operators.

Transpacific eastbound volumes fell 24.5% y/y and contributed with just shy of 50% of the total drop in head-haul and regional volumes vs. 2021. In 2021, September volumes were up 27.4% on 2019 but are now 3.8% lower.

Declining volumes, growing fleet

In total, volumes in September were 1.1 million TEU lower than a year ago and 20 out of 28 region-to-region trades showed negative growth. At the same time, 13 trades recorded lower volumes than in September 2019. Out of the top 10 region-to-region trades which cover nearly 90% of all volumes, the trades into Europe are unsurprisingly doing the worst compared to 2019. The Far East-Europe trade was down 18.8% while the Intra Europe trade declined 11.5%.

The abrupt slowdown in volumes to North America and Europe comes after 9-12 months of the fastest increase on record in business inventories in both the US and the EU. It is therefore likely that the lower volumes reflect a need for businesses to both trim inventories and adjust ongoing imports to expected lower sales as prolonged high inflation is taking a toll on consumers and businesses.

No matter the reason for the low volumes, at this level of volumes, the remaining congestion that has helped to prop-up the supply/demand balance should dissipate quickly. The liner operators will then be left with lower volumes than in 2019, a fleet that has grown 11.8% since then, an orderbook set to add 9.9% to the fleet in 2023, and poor prospects for the global economy. EEXI and CII regulations may absorb as much as 10% of the fleet in 2023, but unless the markets surprise positively, we must still expect to see numerous laid up ships or freight rates that continue to move quickly downwards, or both.

Feedback or a question about this information?

Posted:

09 November 2022

BIMCO's Shipping number of the week

- COVID pandemic wiped 24.6 million TEU off container market growth

- EU tanker import tonne mile demand up 12% as ships avoid Red Sea area

- Demand shocks drive ship recycling to lowest level in 20 years

- 13% of world seaborne trade under attack from Houthis and Somali pirates

- Ships above 12,000 TEU drive 100% increase in average ship size

ELSEWHERE ON BIMCO

Contracts & Clauses

All of BIMCO's most widely used contracts and clauses as well as advice on managing charters and business partners.

Learn about your cargo

For general guidance and information on cargo-related queries.

BIMCO Publications

Want to buy or download a BIMCO publication? Use the link to get access to the ballast water management guide, the ship master’s security manual and many other publications.