Supply/demand balance at 2019 level as container volumes fall 4.6% y/y

Since July 2020, the container market has benefitted from a surge in consumption of goods compared to pre-COVID levels, and head-haul and regional trade volumes have followed. Compared to the same period of 2019, container volumes in the second half of 2020 were up 5.7% while full year 2021 volumes were 9.0% higher. Volumes in the first half of 2022 were up 8.3%, also compared with H1 2019. Despite a growing fleet, capacity supply was unable to keep up as port congestion absorbed as much as 14% of the fleet, data from Sea-Intelligence shows.

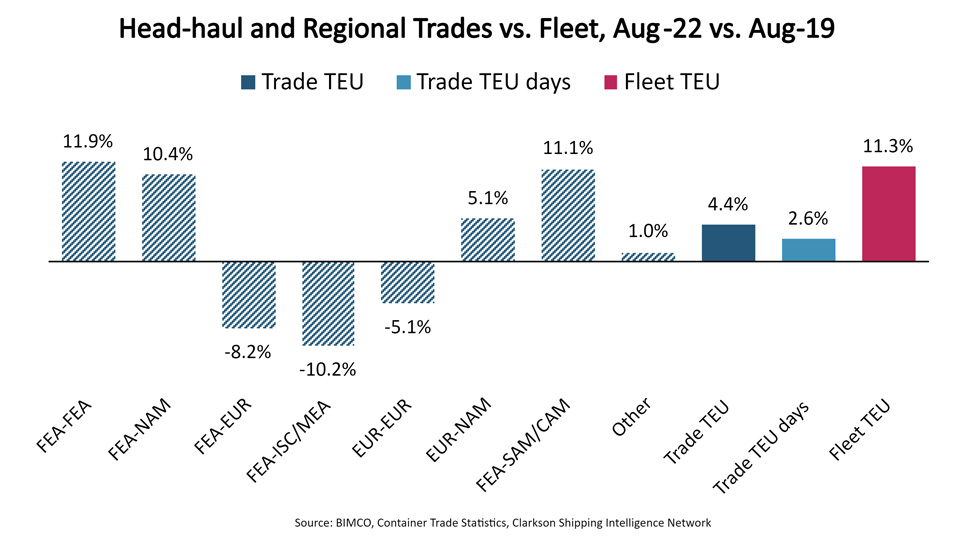

According to new data released by Container Trade Statistics, head-haul and regional trade volumes in August 2022 were at their lowest level since February 2022. The volumes were 3.8% lower than in July and 4.6% lower than August last year, confirming the lack of peak season volumes in key trade lanes. In comparison to pre-COVID volumes in August 2019, the volumes were only 4.4% higher and TEU days were just 2.6% higher due to a change in trade mix.

In August 2022, port congestion absorbed 6-8% more of the fleet than in August 2019. However, the fleet has grown 11.3% since August 2019 and capacity supply was therefore 3-5% higher. As trade TEU days were just 2.6% higher, the vessel supply/demand balance was back at, or just below, 2019 levels.

Despite the weakening of the market, time charter and container freight rates are yet to reach 2019 levels. On average, time charter rates measured by Clarksons have fallen 60% between the peak in April and early October this year, including 55% during the last month alone. Spot container freight rates ex Shanghai measured by Shanghai Shipping Exchange have equally lost about 60% since peaking in January, including a 50% decline during the last two months. However, both remain approximately 2.5 times higher than three years ago.

As expected, time charter rates have responded to the weaker supply/demand balance faster than container freight rates. Through blanked sailings, by closing services, and idling ships, liner operators can reduce supply to meet demand in the freight market whereas this is very difficult in the time charter market. However, liner operators have historically not been very successful at this, except when they have been battling heavy financial losses.

Liner operators have taken steps to reduce supply to better match the weakening demand. According to Sea-Intelligence, blanked sailings in the Transpacific trade during the Golden Week lull added up to 10% more of weekly ship capacity than in a normal year. In addition, a number of liner operators have announced that they are closing Transpacific services. However, so far it has not been enough to stop rates from falling.

Charter ship owners, on the other hand, do not have many tools to adjust supply in the time charter market. Currently, they do benefit from low availability of ships ready for a new time charter contract. During the last two years, many contracts for long periods were concluded which limits ship availability now. In addition, more and more ships appear to be heading to drydock for surveys and to prepare for EEXI and CII regulations. This delays rate reductions but does not protect rates from eventually adjusting fully to the weaker supply/demand balance. Many owners can in the meantime take solace in that the rate reductions do not impact the very high rates in the still active time charter contracts.

As predicted in BIMCO’s 3rd quarter Container Shipping Market Overview and Outlook, lower congestion and weakening volumes are shifting the market downwards, and full “normalisation” of market conditions could be seen later this year or early next year.

Feedback or a question about this information?

Posted:

13 October 2022

BIMCO's Shipping number of the week

- COVID pandemic wiped 24.6 million TEU off container market growth

- EU tanker import tonne mile demand up 12% as ships avoid Red Sea area

- Demand shocks drive ship recycling to lowest level in 20 years

- 13% of world seaborne trade under attack from Houthis and Somali pirates

- Ships above 12,000 TEU drive 100% increase in average ship size

ELSEWHERE ON BIMCO

Contracts & Clauses

All of BIMCO's most widely used contracts and clauses as well as advice on managing charters and business partners.

Learn about your cargo

For general guidance and information on cargo-related queries.

BIMCO Publications

Want to buy or download a BIMCO publication? Use the link to get access to the ballast water management guide, the ship master’s security manual and many other publications.